The War Premium Week

What global markets repriced — and why Pakistan must shift from stabilization to resilience

This was not a classic oil shock. It was a risk shock.

Between February 23 and March 1, global markets experienced a rapid repricing of geopolitical risk following escalating tensions in the Persian Gulf. Oil prices moved, yes. But the bigger movement came in freight rates and war-risk insurance. That is where the real economic story lies, and that is where countries like Pakistan feel the pressure first.

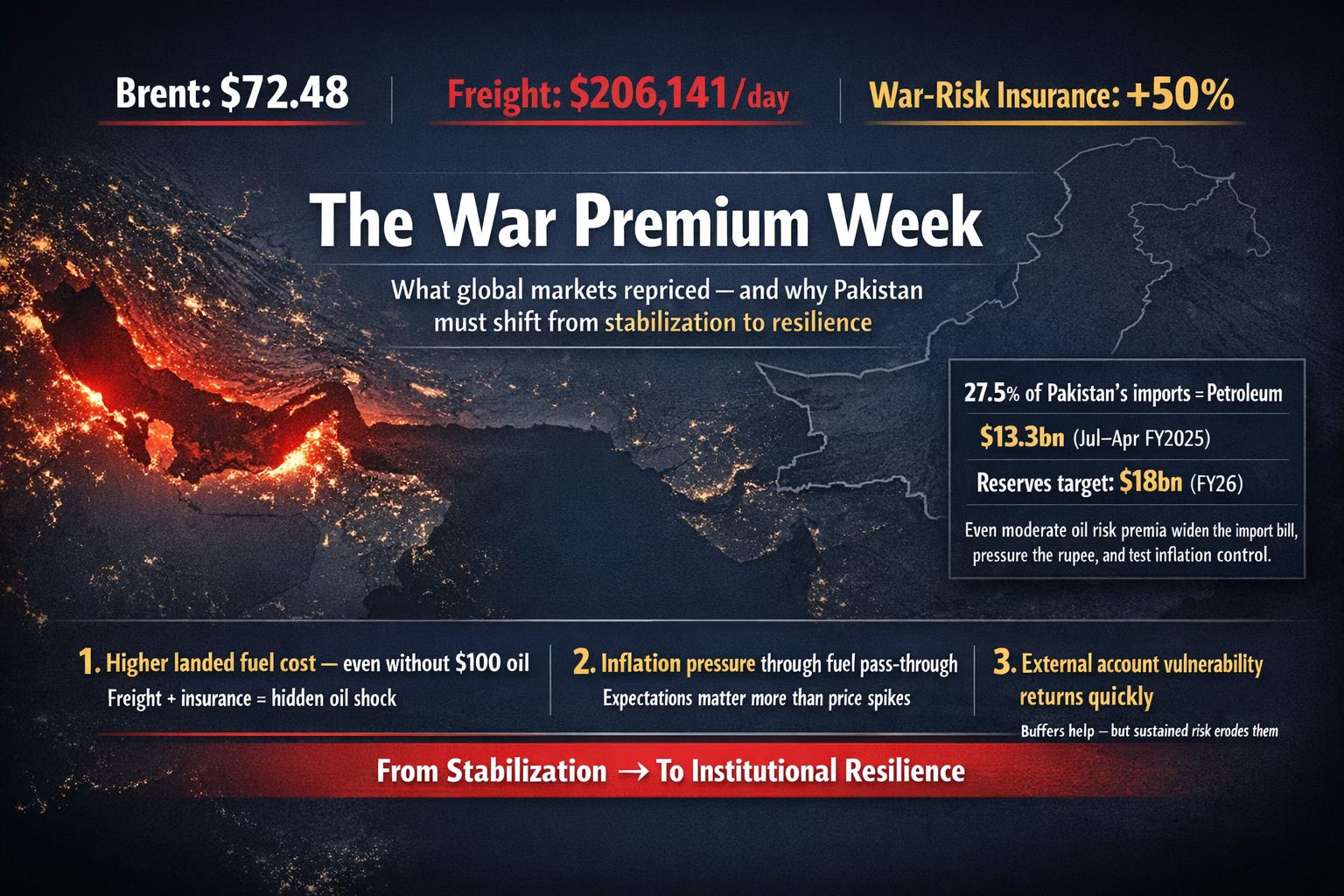

Brent crude settled at $71.49 per barrel on February 23 and closed at $72.48 on February 27. On the surface, that is a modest increase. It does not resemble the dramatic spikes of past oil crises. Yet beneath the benchmark, the cost of moving oil surged. Very Large Crude Carrier (VLCC) freight rates on the Middle East–China route jumped from over $170,000 per day to $206,141 within days. War-risk insurance pricing for a $100 million vessel rose from roughly $250,000 to $375,000 per voyage. That is a 50 percent increase in insurance cost in less than a week.

This is what modern oil shocks look like. They do not always begin with triple-digit crude prices. They begin with uncertainty. They begin with the probability of disruption. And they hit through logistics before they hit through supply shortages.

For Pakistan, this matters enormously. The petroleum group is the country’s largest import category, accounting for 27.5 percent of total imports and $13.3 billion during Jul–Apr FY2025. When freight and insurance premia rise, the landed cost of oil and LNG increases even if Brent remains below $80. The result is a higher import bill, pressure on the current account, and renewed strain on foreign exchange reserves.

Pakistan’s macroeconomic stabilization has improved buffers. The State Bank projects a contained current account deficit and foreign exchange reserves reaching $18 billion by June 2026. That is roughly three months of import cover. It is a cushion, but not a guarantee. Sustained war premia can erode this buffer quickly, especially when capital flows turn cautious.

The transmission channels are clear. First, there is the direct terms-of-trade effect: higher energy import costs widen the external deficit. Second, there is inflation pass-through. Fuel prices affect transport, food distribution, and expectations. Third, there is the financial channel. Research shows that rising geopolitical risks depress equity prices and raise sovereign borrowing costs. Emerging markets face tighter financial conditions precisely when they need liquidity.

Pakistan has already adjusted administered fuel prices upward this week. The key policy question is not whether to pass through higher costs, but how to do so credibly. Delayed adjustments create fiscal pressure. Blanket subsidies distort incentives and undermine stabilization. Sudden, opaque revisions destabilize expectations. A transparent, rules-based pricing mechanism combined with targeted support for vulnerable households is far more stabilizing than political discretion.

The State Bank itself has warned that global commodity prices remain volatile and susceptible to geopolitical developments, with implications for inflation and the external account. This is not a temporary aberration. The Strait of Hormuz, the Druzhba pipeline, Eastern Mediterranean gas fields, these are recurring geopolitical nodes. Markets increasingly price not just actual disruptions but the probability of disruption.

Scenario analysis in global reporting suggests that contained tensions could push oil toward $80, while prolonged escalation could move prices toward $100 and lift global inflation by 0.6–0.7 percentage points. For Pakistan, the difference between $75 and $100 oil is not academic. It is the difference between stabilization and renewed crisis dynamics.

The deeper lesson is institutional. Countries that treat geopolitical shocks as temporary anomalies remain vulnerable. Countries that treat them as structural features build resilience. Mexico’s oil hedging program is a documented example of institutional risk management. The World Bank Treasury provides advisory services on commodity price risk management to developing countries. Strategic reserves, fiscal rules, and automatic stabilizers are not luxuries; they are shock absorbers.

Pakistan must move in this direction. An energy price risk unit with a clear hedging mandate, transparent fuel pricing rules, a formal reserve adequacy framework, accelerated export diversification, and a credible fiscal rule would reduce vulnerability to repeated shocks. These reforms are technical, not ideological. They convert volatility into manageable risk.

This week’s lesson is blunt. The fastest-moving price was not crude oil. It was risk. Freight surged. Insurance premiums spiked. Markets turned defensive. That is how modern geopolitics transmits into inflation and external stress.

Pakistan’s challenge is no longer simply stabilization. It is resilience. In an era where chokepoints move markets overnight, macroeconomic strength will depend less on reacting to crises and more on designing institutions that do not break when crises arrive.

The next oil shock may not come with dramatic headlines. It may come quietly, through higher freight invoices and insurance quotes. The real reform question is whether Pakistan chooses to treat this week as an episode or as a warning.